Purchase journal Wikipedia

Following the Panic of 1893, Chattanooga Times publisher Adolph Ochs gained a controlling interest in the company. In 1935, Ochs was succeeded by his son-in-law, Arthur Hays Sulzberger, who began a push into European news. Sulzberger’s son-in-law Arthur Ochs became publisher in 1963, adapting to a changing newspaper industry and introducing radical changes. Supreme Court case New York Times Co. v. Sullivan, which restricted the ability of public officials to sue the media for defamation.

Authoritatively ranked lists of books sold in the United States, sorted by format and genre.

This entry reflects the acquisition of inventory without the immediate outlay of cash, increasing both the company’s assets (inventory) and liabilities (accounts payable). Journal entries are recorded in the “journal”, also known as “books of original entry”. A journal entry is made up of at least one account that is debited and at least one account credited.

Purchases Journal Proof of Postings

The method of payment (cash or credit) influences which accounts are involved in the transaction. This account will be credited with every transaction we record in this journal. The other account where we will record a balancing debit entry will be the Office Supplies account.

Explanation for Credit Purchase

In addition, the company incurred in an obligation to pay $400 after 30 days. That is why we credited Accounts Payable (a liability account) in the above entry. A journal, also known as Books of Original Entry, keeps records of business transactions in a systematic order.

An inventory purchase journal entry records the acquisition of goods that a business intends to sell. This entry typically involves debiting the Inventory account to increase the company’s assets, showing that inventory has been added to the stock. Any transaction entered into the purchases journal involves a credit to the accounts payable account and a debit to the expense or asset account to which a purchase relates. For example, the debit relating to a purchase of office supplies would be to the supplies expense account.

Example of Inventory Purchase Journal Entry

- Sulzberger’s son-in-law Arthur Ochs became publisher in 1963, adapting to a changing newspaper industry and introducing radical changes.

- On March 16th, Power Tools purchased inventory on account from Brown Manufacturing for $4,345.

- It can also help you keep an accurate inventory of the products and services you offer.

- This is one of the basics books in the bookkeeping process, which is essential in preparing ledger balances, trial balance, and final accounts.

- All of our content is based on objective analysis, and the opinions are our own.

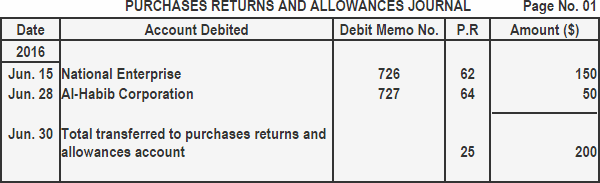

In cases where the goods supplied do not match the description or have quality issues or damage, the purchaser has to return them to the supplier. Then the supplier will issue a Credit Note document, which will be adjusted against the payments of goods in the future. For example, X Ltd. returned goods worth $1,000, and Y Ltd. issued a credit note for that value. So next time X Ltd. will purchase $5,000, it only has to pay $4,000 as $1,000 will be adjusted against credit note.

This increases the inventory, reflecting the addition of gardening tools. Initially, the details of the inventory purchase, including the quantity, price, and terms of sale, are determined. Sometimes, the entity internal revenue also includes other information related to purchasing like fixed assets, inventories, or expenses. Finance Strategists has an advertising relationship with some of the companies included on this website.

Once the order has arrived, they will check that it matches the required description and quantity matches what was requested. Once the purchasing department confirms that goods have been received, the invoice goes to accounts for payment. Inventory purchases represent the acquisition of goods that a business intends to sell. These transactions not only affect the company’s current assets but also have implications for its cost of goods sold (COGS) and, ultimately, its gross profit. The subsidiary (customer) ledgers would be updated daily but at the end of the period, the TOTALS only would be recorded in posted directly into the accounts listed with no journal entry necessary. It is also known as a Purchase journal, Invoice book or Purchase daybook.

However, the payment terms are not specified in our example, so we are going to leave this section blank, as well as the reference number, which we are going to get after we post all transactions into the ledger. The two accounts involved in this transaction will get respective debit and credit entries. The purchase transaction journal entries below act as a quick reference, and set out the most commonly encountered situations when dealing with the double entry posting of purchase transactions.